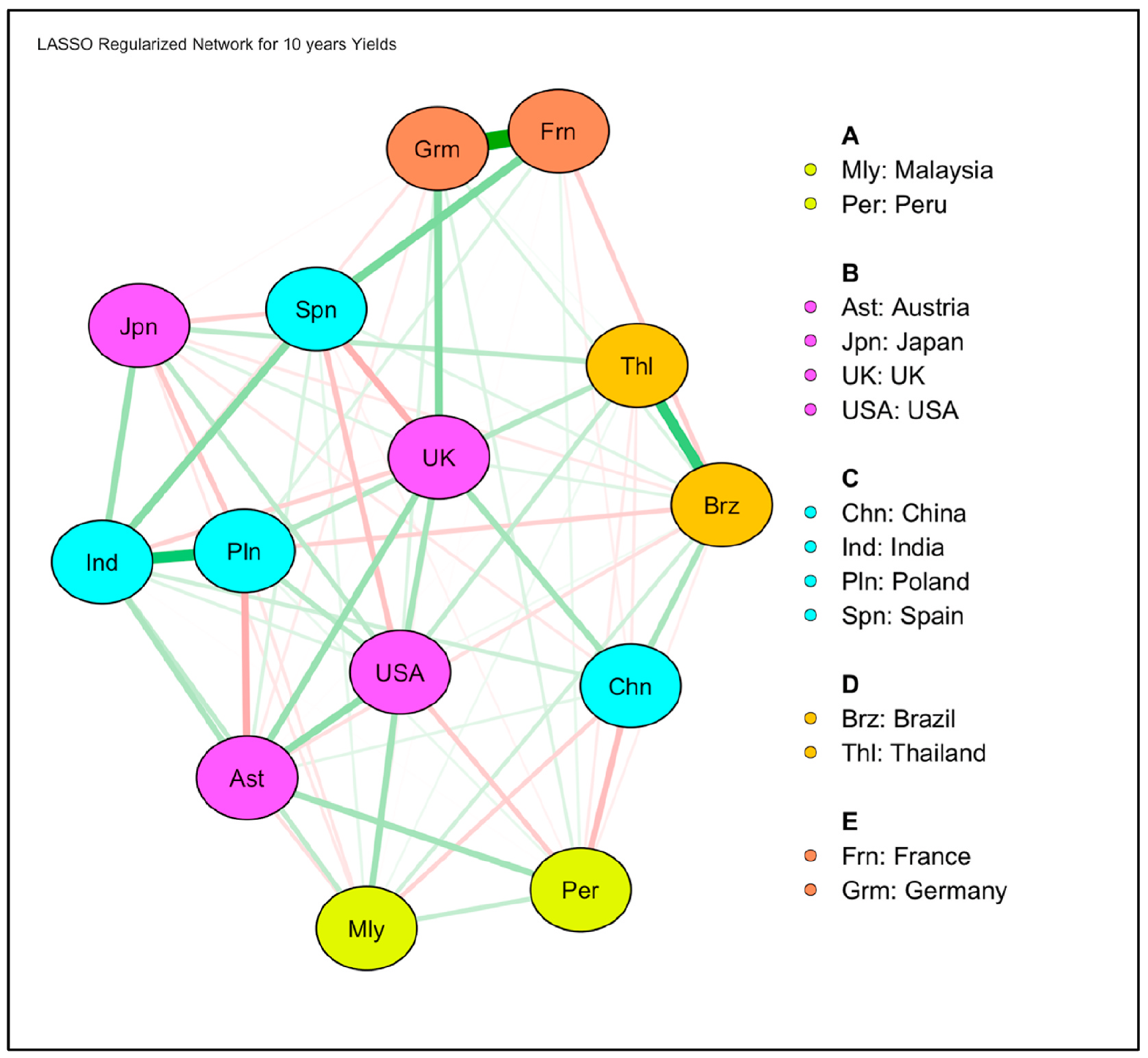

| Using daily yield data of 14 sovereign bond markets from emerging and developed

economies from July 10, 2000, to July 10, 2022, we examine their scaling properties using generalized

Hurst exponent and spectral density analysis and investigate the connectedness based on a network analysis

approach. We consider the yields of 2-year and 10-year bond yields to investigate the scaling properties

for short- and long-term sovereign bonds. This selection also allows us to examine sovereign bond spreads

with respect to the USA. We also use regularized partial correlation network analysis to connect different

countries in communities based on yields. We find that the scaling behavior of the bond yields for both

terms fits well using the Hurst exponent and spectral analysis confirms this finding. Moreover, we also

find that even though bonds in both cohorts show anti-persistent behavior except that of the USA, the

developed economies’ bond yields are relatively less anti-persistent as compared to those of emerging

economies. The networks of both the 2-year and 10-year yields indicate community formation in various

countries which provides diversification benefits to the investors. Most of the emerging countries are

classified into one community in the long-tenure bonds as well but this concentration is more evident in

the short-tenure bonds. |